|

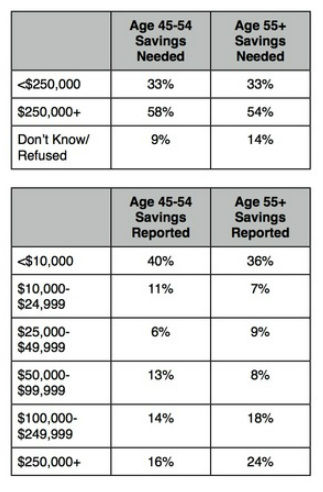

3/28/2013 0 Comments Savings Expectations vs. Reality Stormy skies for retirement savings? For the last few years, retirement confidence has been at or near historically low levels. Even as reports of a rebounding economy surface, confidence continues to remain low. Perhaps one explanation for this is apparent in the data reported in the annual Retirement Confidence Survey (RCS) conducted by the Employee Benefit Research Institute (EBRI) and Mathew Greenwald & Associates. When you look at the retirement savings expectations of workers and then compare this to actual savings, there is a very significant gap. For example, let's consider the age groups closest to retirement. For those ages 45 to 54, as well as those age 55 and above, more than half think that they will need $250,000 or more in savings and investments for a secure retirement (excluding housing and defined benefit plans). While those 55 and above may still have some working years to accumulate additional retirement savings, and those in the 45-54 bracket even more years, the red flag is that more than half of both demographic groups have less than $50,000 in savings reported. The end result is that people now expect to work longer. A decade ago in 2003, 24% of those in the 45-54 bracket expected to retire at age 66 or later; in 2013, that figure is up to 35%. Similarly, in 2003, 29% of those 55 or older thought that they would retire at age 66 or later; that has risen to 44%. What is worrisome is that even if more individuals plan to work longer to overcome the savings shortfalls, in reality, more than half have retired sooner than expected due to adverse circumstances such as health problems or disability. (Numbers in tables below are from the RCS and may be >100% due to rounding.)

0 Comments

Sarasota Sunset Silhouette Despite recent reports of improving economic trends, the latest version of the Retirement Confidence Survey (RCS) reinforces that confidence in having a secure retirement remains at historicaly low levels. According to the annual survey from the Employee Benefit Research Institute (EBRI) and Mathew Greenwald & Associates, 28% of those still working are "not at all confident" and 21% are "not too confident". For thoe who have already retired, only 18% are "very confident", while 14% are "not at all confident".

In my blog last week and in my first entry last July, I suggested that the key to resolving the retirement savings quandary is to understand that participants realize that saving for retirement is important, but other, more immediate financial priorities and challenges are standing in the way. The 2013 RCS results confirm this. According to the RCS, "Retirement savings may be taking a back seat to more immediate financial concerns." An almost microscopic 2% of workers and 4% of retirees consider saving for retirement to be the most pressing financial issue facing most Americans. By contrast, 30% of workers and 27% of retirees point to job uncertainty, while 12% of both workers and retirees cite making ends meet. The high cost of living and day-to-day expenses are the primary reasons eligible employees don't contribute more or at all to their employer's retirement plan. Another key obstacle is debt, with 55% of workers and 39% of retirees having difficulties in this area. One end result is that people now expect to retire much later than they once did. Back in 1991, only 11% of workers expected to retire after age 65. In 2013, that figure has jumped to 36% - and 7% don't expect to retire at all. What does all of this mean? I would suggest that it is imperative that we focus on the individual's complete financial circumstances. Saving for retirement does not occur in a vacuum. Automatic features are wonderful for helping people on the road to a more secure retirement, but the road has many obstacles as well. Perhaps some combination of these automatic features and tools to help overcome other financial challenges is what the doctor ordered.  Big picture: snow & ice give way to leaves in a few weeks Big picture: snow & ice give way to leaves in a few weeks Back in July of last summer when I first started this blog, I made the simple suggestion that the main reason individuals were not saving more for retirement was due primarily to conflicting financial priorities. In other words, people understood the importance of retirement savings, but other priorities were getting in the way.

An important new report by Deloitte seems to lend credence to this thought. According to the Deloitte report, Meeting the Retirement Challenge: New Approaches and Solutions for the Financial Services Industry, the biggest barrier in taking the right steps to prepare for a secure retirement is that "(w)hile retirement is a leading concern for a majority of the survey respondents, many cited difficulty balancing such long-term needs with other, often more immediate financial priorities." Communications from financial institutions often neglect to consider the individual's entire financial picture, complete with other priorities. Deloitte believes that taking a more holistic, integrated approach to retirement planning will be a key step in enabling more individuals to be better prepared for retirement. Retirement needs would be "addressed early in a customer's lifecycle, but in conjunction with other financial priorities." The Deloitte survey found that 46% say they do not have enough disposable income to allocate to retirement savings. Additionally, while the survey did reveal that saving for retirement was generally the top or second-highest priority, competing financial priorities such as a mortgage, student loan, or other debt were the biggest obstacles to successful saving. In fact, for those with 15+ years to go until anticipated retirement, 55% considered competing financial priorities to be the biggest obstacle to not having a formal plan for retirement. Similarly, 45% of those with 5-15 years to go said the same thing. The report looks at other factors as well, such as healthcare costs, lack of trust in financial institutions, and the belief that savings will be inadequate despite best efforts, but the finding that the big picture must indeed look at the complete financial picture of the individual is a critical missing piece of the retirement savings puzzle. Deloitte recommends that financial service providers take heed of this holistic approach: "It likely does little good to pitch retirement products alone to someone who is more concerned for the moment with mortgage or other debt issues." The Transamerica Center for Retirement Studies has released a report that generally finds that women face greater obstacles than men in achieving retirement security, in large measure due to the balancing act of meeting current and future needs. According to Transamerica, some of the contributing factors include:

Almost one third of the women surveyed expect to provide financial support for family members when retired. Current financial challenges, such as paying off credit card debt, are seen as getting in the way. Transamerica notes a concern that only one in five women have a backup plan if forced into retirement earlier due to job loss, health problems, or some other factor. Women estimate their retirement savings needs at a median of $500,000, versus men, who place the figure at $750,000. Both of these figures, however, are many times higher than the $77,300 average account balance recently reported by Fidelity or the just under $60,000 average estimated by EBRI. Additional details and recommendations from the Transamerica report are available on its website.  Better savings on the horizon for some Intuitively, it makes sense that those individuals who are saving for retirement via both a 401(k) plan and an IRA may have more success than those saving in just a 401(k) or IRA alone. What is interesting is new data from Fidelity quantifying just how substantial the impact is of having both types of plans. As of 12-31-2012, the average balance in 401(k) plans serviced by Fidelity was $77,300. This represents over 20,000 plans with about 12 million participants . For the nearly one million participants who also maintain an IRA with Fidelity, the average account balance jumped to over $225,000. (Those participating in 403(b) programs also are included in the statistics.) For those age 65-69, the average account balance was just under $400,000, a very encouraging sign. Benefiting from the catch-up rules, savers in their 50's contributed an average of $13,100 annually. A Fidelity news release provides additional details. A note of caution, however - the flip side is that there are millions of participants for whom saving in both is difficult at best and virtually impossible at worst.

|

Blog Author - Ken FelsherWith over 25 years of writing, editing, and research experience. I enjoy sharing with my readers my love of working with content on a variety of subjects.

CategoriesAll 401(k) 402(g) Boomers Catch-up DB Dc Deferral Limit Defined Benefit Defined Contribution ERISA Healthcare Participation Pension Professionally Managed RCS Retirement Retirement Confidence Tax Code Vanguard Women Working Archives

March 2015

|